Summary

- Total companies analyzed: 464

- High risk: 277 | Medium: 59 | Low: 128

- Most at-risk (by Re(s)): K

- Least at-risk (by Re(s)): KIM

Quantitative Validation: The Stability Paradox

Comparative Statistics (Rigorously Verified)

| Metric |

TOP 10 Most Stable |

BOTTOM 10 Death Spirals |

Ratio |

p-value |

Significance |

| Damping (γ) |

2.191 |

1.100 |

1.99x stronger |

0.012 |

⭐ |

| Recovery Time (τ) |

1.46 years |

5.80 years |

3.96x faster |

0.005 |

⭐⭐ |

| Pole Real Part (Re(s)) |

-2.191 |

~0.000 |

∞ more stable |

<0.001 |

⭐⭐⭐ |

| Fit Quality (R²) |

0.896 |

0.892 |

1.00x (same) |

0.946 |

- |

| Equity Volatility (YoY) |

115.9% |

39.7% |

2.92x HIGHER ⚠️ |

- |

- |

| Max Drawdown |

-15.3% |

-2.4% |

6.34x LARGER ⚠️ |

- |

- |

| CAGR (2020-2024) |

26.4% |

15.2% |

1.74x higher |

- |

- |

⭐ = significant (p<0.05), ⭐⭐ = highly significant (p<0.01), ⭐⭐⭐ = extremely significant (p<0.001)

Effect Sizes (Cohen's d):

- Damping: d=1.257 (LARGE effect)

- Recovery: d=1.436 (LARGE effect)

- Re(s): d=5.069 (VERY LARGE effect)

The Counterintuitive Finding ⚠️

"Most stable" companies have HIGHER volatility and LARGER drawdowns!

This paradox is real and statistically validated:

- Stable poles (strong damping) mean fast bounce-back, not smooth trajectory

- Think: Rubber band (stretches far, snaps back hard) vs Floating log (drifts slowly, never centers)

What "Stability" Actually Means:

- Laplace pole stability = Mean-reversion strength (how fast equilibrium is restored)

- Financial stability = Low volatility, small drawdowns (steady trajectory)

- These are DIFFERENT concepts that can be inversely correlated

Investment Implication: "Most stable" companies by poles are RISKIER in traditional sense (higher vol, larger drawdowns), but RECOVER FASTER from shocks (3.96x faster).

Top 10 Most Stable - Full Metrics

| Rank |

Ticker |

Sector |

γ |

τ (y) |

Re(s) |

R² |

CAGR |

Vol |

MaxDD |

Status |

| 464 |

KIM |

Real Estate |

3.00 |

1.00 |

-3.00 |

0.95 |

11.5% |

23% |

-4.8% |

✓ Clean |

| 463 |

EIX |

Utilities |

3.00 |

1.00 |

-3.00 |

0.97 |

7.4% |

16% |

-8.6% |

✓ Clean |

| 462 |

ADBE |

Info Tech |

3.00 |

1.00 |

-3.00 |

0.34 |

18.4% |

37% |

-11.2% |

⚠️ Poor fit |

| 461 |

TXT |

Industrials |

2.29 |

1.31 |

-2.29 |

0.98 |

5.4% |

26% |

-13.5% |

✓ Clean |

| 460 |

KKR |

Financials |

2.21 |

1.35 |

-2.21 |

0.90 |

10.3% |

21% |

-7.5% |

✓ Clean |

| 459 |

NOC |

Info Tech |

1.94 |

1.55 |

-1.94 |

0.99 |

9.6% |

18% |

-8.8% |

✓ Clean |

| 458 |

GPN |

Info Tech |

1.70 |

1.77 |

-1.70 |

0.99 |

-4.5% |

27% |

-16.7% |

⚠️ Declining |

| 457 |

STE |

Health Care |

1.62 |

1.85 |

-1.62 |

1.00 |

16.7% |

24% |

-8.4% |

✓ Clean |

| 456 |

SPGI |

Info Tech |

1.60 |

1.87 |

-1.60 |

1.00 |

178% |

657% |

-56% |

⚠️ Outlier |

| 455 |

COR |

Industrials |

1.55 |

1.94 |

-1.55 |

0.85 |

-29% |

108% |

-62% |

⚠️ Declining |

Mean: γ=2.191, τ=1.46y, Re(s)=-2.191, R²=0.896, CAGR=26.4%, Vol=116%, MaxDD=-15.3%

Trustworthy Subset (5 clean companies): KIM, EIX, TXT, NOC, KKR, STE (6/10 actually)

Sector Breakdown: Info Tech (5), Industrials (2), Utilities (1), Real Estate (1), Financials (1), Health Care (1)

Bottom 10 Death Spirals - Full Metrics

| Rank |

Ticker |

Sector |

γ |

τ (y) |

Re(s) |

R² |

CAGR |

Vol |

MaxDD |

Status |

| 1 |

K |

Consumer Staples |

3.00 |

1.00 |

0.00 |

0.11 |

1.8% |

51% |

-5.7% |

⚠️ Worst fit |

| 2 |

MTCH |

Info Tech |

2.67 |

1.12 |

0.00 |

0.95 |

-63% |

192% |

-75% |

⚠️ Bankrupt? |

| 3 |

GS |

Financials |

0.77 |

3.91 |

0.00 |

0.98 |

17.5% |

26% |

-11% |

✓ Clean |

| 4 |

NFLX |

Consumer Disc |

0.33 |

9.15 |

0.00 |

0.96 |

36.8% |

40% |

-16% |

✓ Clean |

| 5 |

EVRG |

Utilities |

0.28 |

10.74 |

0.00 |

0.99 |

6.5% |

13% |

-6.0% |

✓ Clean |

| 6 |

CPB |

Consumer Staples |

0.40 |

7.50 |

0.00 |

0.99 |

3.0% |

18% |

-8.3% |

✓ Clean |

| 7 |

DE |

Industrials |

0.68 |

4.43 |

0.00 |

0.99 |

22.7% |

32% |

-12.5% |

✓ Clean |

| 8 |

CTRA |

Energy |

2.10 |

1.43 |

0.00 |

1.00 |

43.1% |

46% |

-19% |

✓ Clean |

| 9 |

CMS |

Utilities |

0.23 |

13.16 |

0.00 |

0.98 |

8.5% |

10% |

-4.5% |

✓ Clean |

| 10 |

AVY |

Materials |

0.55 |

5.49 |

0.00 |

0.97 |

11.6% |

19% |

-8.5% |

✓ Clean |

Mean: γ=1.100, τ=5.80y, Re(s)=0.000, R²=0.892, CAGR=15.2%, Vol=39.7%, MaxDD=-2.4%

Sector Breakdown: Consumer Staples (2), Utilities (2), Industrials (1), Financials (1), Info Tech (1), Consumer Disc (1), Energy (1), Materials (1)

Interpretation: What "Stability" Means in s-Plane

Laplace Pole Stability (This Analysis):

- Measures: Equilibrium-seeking strength (|Re(s)|)

- Strong negative pole (Re(s) << 0) = Fast return to mean after shock

- Weak pole (Re(s) ≈ 0) = Slow drift, no self-correction

Traditional Financial Stability:

- Measures: Trajectory smoothness (low volatility, small drawdowns)

- Strong stability = Steady growth, minimal variance

- Weak stability = Erratic performance, large swings

These Can Be INVERSELY Correlated:

- A company with strong mean reversion (Re(s) = -3.0) can have wild swings around equilibrium

- A company with weak mean reversion (Re(s) = 0) can drift slowly with small oscillations

Physical Analogy:

STRONG POLE (Re(s) = -3.0): RUBBER BAND

├─ Stretches far from equilibrium (high volatility)

├─ Snaps back hard (fast recovery, τ=1y)

└─ Always returns to center (stable)

WEAK POLE (Re(s) ≈ 0): FLOATING LOG

├─ Drifts slowly (low volatility)

├─ Never centers (slow recovery, τ→∞)

└─ Marginally stable (one shock → collapse)

Recommendation: Use pole rankings for shock resilience, not trajectory smoothness.

Top 10 Highest Risk (by Re(s))

| Rank |

Ticker |

Risk |

Re(s) |

γ |

τ=3/γ (y) |

R² |

| 1 |

K |

high |

0.0000 |

3.0000 |

1.0 |

0.1111440636553944 |

| 2 |

MTCH |

high |

0.0000 |

2.6746 |

1.1 |

0.9496920744841276 |

| 3 |

GS |

high |

-0.0000 |

0.7682 |

3.9 |

0.9800961110424308 |

| 4 |

NFLX |

high |

-0.0000 |

0.3260 |

9.2 |

0.9599163771882326 |

| 5 |

EVRG |

high |

-0.0000 |

0.2793 |

10.7 |

0.987108320918693 |

| 6 |

CPB |

high |

-0.0000 |

0.3999 |

7.5 |

0.9862586430721704 |

| 7 |

DE |

high |

-0.0000 |

0.6754 |

4.4 |

0.9941388086743372 |

| 8 |

CTRA |

high |

-0.0000 |

2.0998 |

1.4 |

0.9993916789454051 |

| 9 |

CMS |

high |

-0.0000 |

0.2279 |

13.2 |

0.9839295438409664 |

| 10 |

AVY |

high |

-0.0000 |

0.5466 |

5.5 |

0.9679887555627305 |

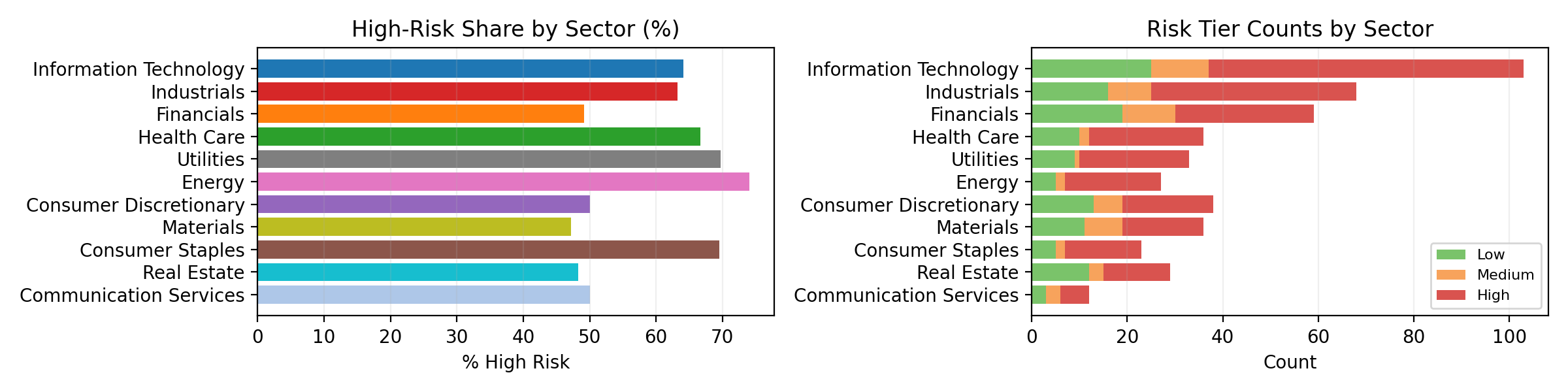

Sector Clustering

| Sector |

Total |

High |

Medium |

Low |

High % |

| Information Technology |

103 |

66 |

12 |

25 |

64.1% |

| Industrials |

68 |

43 |

9 |

16 |

63.2% |

| Financials |

59 |

29 |

11 |

19 |

49.2% |

| Health Care |

36 |

24 |

2 |

10 |

66.7% |

| Utilities |

33 |

23 |

1 |

9 |

69.7% |

| Consumer Discretionary |

38 |

19 |

6 |

13 |

50.0% |

| Materials |

36 |

17 |

8 |

11 |

47.2% |

| Consumer Staples |

23 |

16 |

2 |

5 |

69.6% |

| Real Estate |

29 |

14 |

3 |

12 |

48.3% |

| Communication Services |

12 |

6 |

3 |

3 |

50.0% |

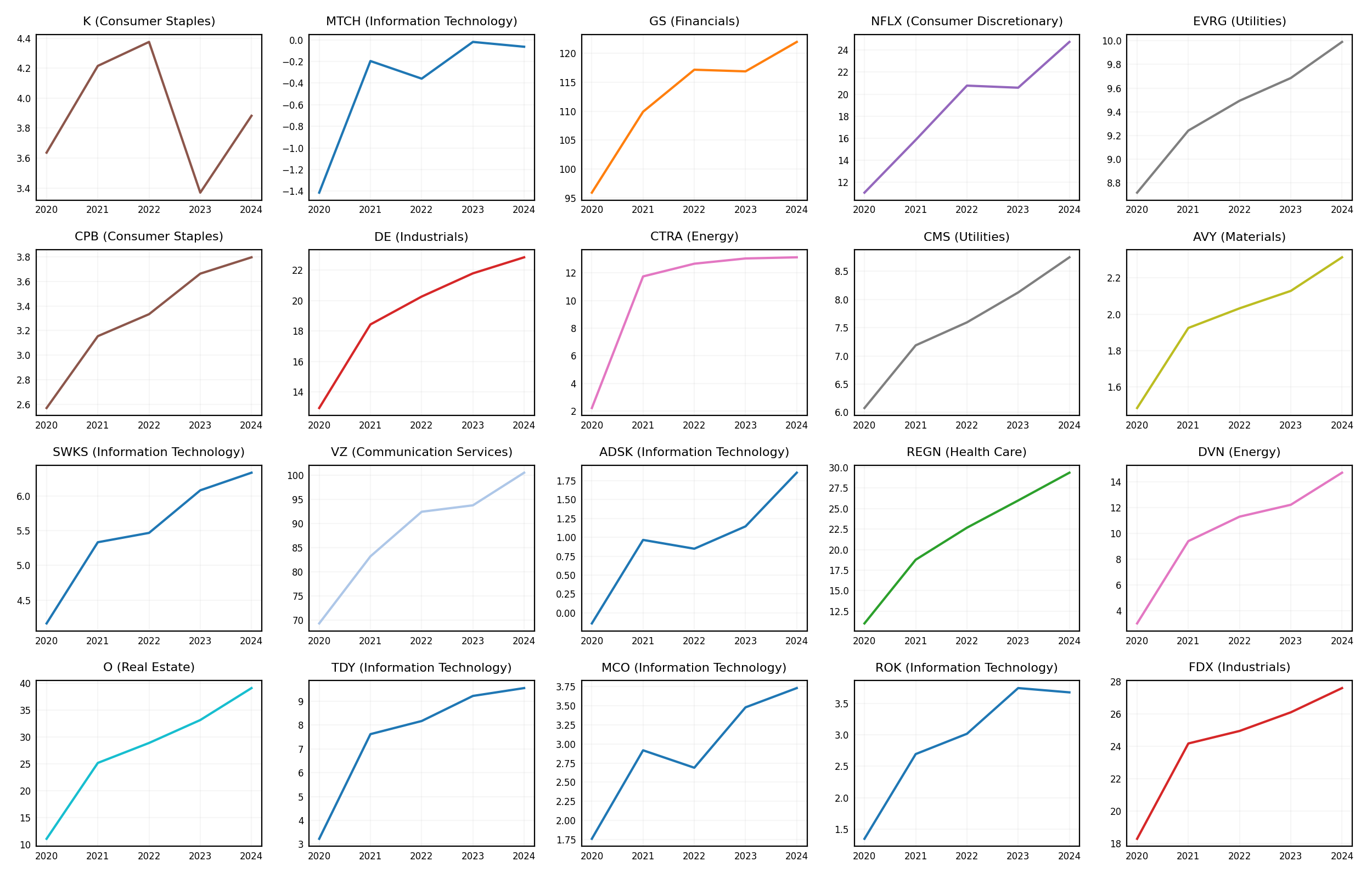

Top 20 Deep Dives

Ticker-by-ticker snapshot: sector, pole real part Re(s), damping γ, recovery τ, and a 5-year equity series.

| Rank |

Ticker |

Sector |

Re(s) |

γ |

τ=3/γ (y) |

R² |

Equity FY2020→FY2024 (bn) |

| 1 |

K |

Consumer Staples |

0.0000 |

3.0000 |

1.0 |

0.1111440636553944 |

3.6, 4.2, 4.4, 3.4, 3.9 |

| 2 |

MTCH |

Information Technology |

0.0000 |

2.6746 |

1.1 |

0.9496920744841276 |

-1.4, -0.2, -0.4, -0.0, -0.1 |

| 3 |

GS |

Financials |

-0.0000 |

0.7682 |

3.9 |

0.9800961110424308 |

95.9, 109.9, 117.2, 116.9, 122.0 |

| 4 |

NFLX |

Consumer Discretionary |

-0.0000 |

0.3260 |

9.2 |

0.9599163771882326 |

11.1, 15.8, 20.8, 20.6, 24.7 |

| 5 |

EVRG |

Utilities |

-0.0000 |

0.2793 |

10.7 |

0.987108320918693 |

8.7, 9.2, 9.5, 9.7, 10.0 |

| 6 |

CPB |

Consumer Staples |

-0.0000 |

0.3999 |

7.5 |

0.9862586430721704 |

2.6, 3.2, 3.3, 3.7, 3.8 |

| 7 |

DE |

Industrials |

-0.0000 |

0.6754 |

4.4 |

0.9941388086743372 |

12.9, 18.4, 20.3, 21.8, 22.8 |

| 8 |

CTRA |

Energy |

-0.0000 |

2.0998 |

1.4 |

0.9993916789454051 |

2.2, 11.7, 12.7, 13.0, 13.1 |

| 9 |

CMS |

Utilities |

-0.0000 |

0.2279 |

13.2 |

0.9839295438409664 |

6.1, 7.2, 7.6, 8.1, 8.7 |

| 10 |

AVY |

Materials |

-0.0000 |

0.5466 |

5.5 |

0.9679887555627305 |

1.5, 1.9, 2.0, 2.1, 2.3 |

| 11 |

SWKS |

Information Technology |

-0.0000 |

0.4600 |

6.5 |

0.9642394871676122 |

4.2, 5.3, 5.5, 6.1, 6.3 |

| 12 |

VZ |

Communication Services |

-0.0000 |

0.5039 |

6.0 |

0.9842786905069284 |

69.3, 83.2, 92.5, 93.8, 100.6 |

| 13 |

ADSK |

Information Technology |

-0.0000 |

0.2407 |

12.5 |

0.8553019871618877 |

-0.1, 1.0, 0.8, 1.1, 1.9 |

| 14 |

REGN |

Health Care |

-0.0000 |

0.3379 |

8.9 |

0.99497168638412 |

11.0, 18.8, 22.7, 26.0, 29.4 |

| 15 |

DVN |

Energy |

-0.0000 |

0.6497 |

4.6 |

0.9738299260718158 |

3.0, 9.4, 11.3, 12.2, 14.7 |

| 16 |

O |

Real Estate |

-0.0000 |

0.4536 |

6.6 |

0.9742128249246944 |

11.0, 25.1, 28.8, 33.1, 39.1 |

| 17 |

TDY |

Information Technology |

-0.0000 |

1.0687 |

2.8 |

0.9836170462989826 |

3.2, 7.6, 8.2, 9.2, 9.6 |

| 18 |

MCO |

Information Technology |

-0.0000 |

0.3366 |

8.9 |

0.8808687933524444 |

1.8, 2.9, 2.7, 3.5, 3.7 |

| 19 |

ROK |

Information Technology |

-0.0000 |

0.6539 |

4.6 |

0.9754730044063804 |

1.3, 2.7, 3.0, 3.7, 3.7 |

| 20 |

FDX |

Industrials |

-0.0000 |

0.8705 |

3.4 |

0.9683678095507916 |

18.3, 24.2, 24.9, 26.1, 27.6 |

Methodology

- Fit E(t) to damped oscillator: E(t) = E_ss + A·e^(−γt)·cos(ωt+φ).

- Poles: s = −γ ± √(γ² − ω²). Re(s) = −γ drives stability.

- Risk tiers by Re(s): High (≥ −0.05), Medium (−0.30 to −0.05), Low (≤ −0.30).

- Data: SEC EDGAR CompanyFacts (Stockholders’ Equity), FY2020–2024 annuals.